![]()

The Free Market Center

![]()

A widely held belief exists that dollars are always money. This belief leads to the erroneous assumption that the Federal Reserve controls the quantity of money in the US economy. I will show you that people do not use all dollars as money. Following my usual practice, I will post a definition of money to use as a reference point:

"Money" consists of any economic good, or any claim on such a good, that serves as a general medium of indirect exchange and that acts as a final means of payment.

I have seen businessmen who frame their “first dollar” and hang it on the wall. I have eaten a few times at a restaurant in which customers scribble various comments and images on dollar bills, and the restaurant posts them on the walls. People do not use any of these dollars as money. The use of an economic good or claim determines whether it fits the definition of money or not. The word “money” does not ascribe an intrinsic quality to anything we refer to as “dollars.”

The same holds for the dollars held by banks as reserves. Dollars held as reserves and the dollar-denominated claims of bank customers cannot both be used as money and reserves simultaneously. This statement is true whether the bank holds its reserves in its vault or at the Federal Reserve Bank.

I will, from here on out, refer to dollars held as reserves as reserve dollars (or R-dollars) and dollar-denominated deposit liabilities as money dollars (or M-dollars).

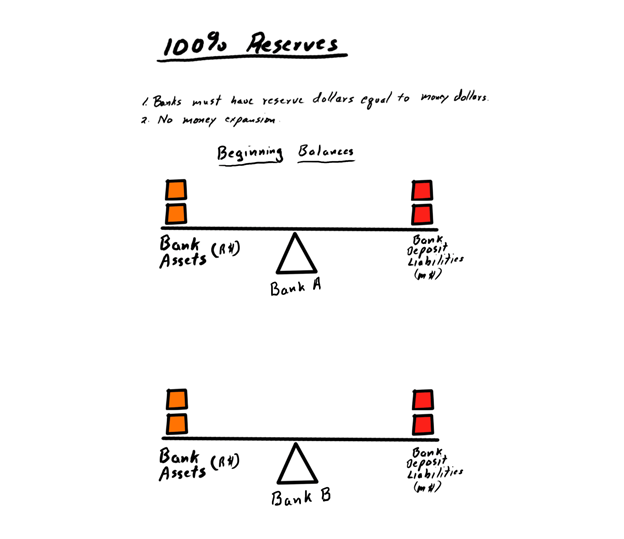

To demonstrate the relationship between bank reserves (R-dollars) and demand deposit liabilities (M-dollars), I will show a graphic representation of a banking system with a 100% reserve requirement.

A 100% reserve requirement means that banks must have at least 1 R-dollar in “reserve” for every M-dollar in deposit liabilities.

For simplicity, this banking system has only two banks — Bank A and Bank B.

In the beginning, both banks have the same amount of dollars of reserves and dollar deposit liabilities. As a bank customer, you only care about the deposit liabilities, which people normally refer to as “bank deposits.”

Because the bank must have a number of reserve dollars equal to the number of money dollars, the number of R-dollars on one side of the balance equals the number of M-dollars on the other side of the balance.

In this system, how do M-dollars get “transferred” from Bank A to Bank B?

If your neighbor John, who has an account at Bank A, buys a wheelbarrow for 25 M-dollars from you, who has an account at Bank B, how do those dollars get “transferred” from John’s bank (Bank A) to your bank (Bank B)?

The “transfer” of 25 M-dollars from Bank A to Bank B occurs as the result of two separate simultaneous transactions. I will assume, for the sake of this example, that the Federal Reserve Bank holds all reserves.

In the first transaction the Federal Reserve reduces the account of Bank A by 25 R-dollars. Simultaneously they increase the account of Bank B by 25 R-dollars.

At the same time, Bank A reduces its liability to John by 25 M-dollars. Bank B increases its deposit liability to you by 25 M-dollars.

![]()

These transactions remain separate but keep the number of M-dollars equal to the number of R-dollars. Total R-dollars in the Fed remains the same and the aggregate of M-dollars also remains the same. The 25 R-dollars have been deleted from the account of Bank A and added to the account of Bank B. Also, the 25 M-dollars get expunged in John’s deposit liability account in Bank A, and 25 M-dollars get created in your deposit liability account in Bank B.

I have attempted to make this example as simple as possible to illustrate the important fact that the R-dollars never leave the Fed.

In spite of what you may hear from other sources, the Fed does not create “money.” It can only create and destroy R-dollars. Likewise, the creation and destruction of M-dollars remains under the control of banks.

I will use this essay as a jumping-off point to explain the more complex transactions within a fractional reserve banking system.

© 2010—2020 The Free Market Center & James B. Berger. All rights reserved.

To contact Jim Berger, e-mail: